Things in State College are good. I have previewed on this blog that I am establishing a new advisory firm, in addition to my consultancy with ThorCo. My partner and I have been adding some nice clients and are pleased to see the pipeline full from our own relationships and referrals from past clients and friends. I am having as much fun in my professional life now as I ever have.

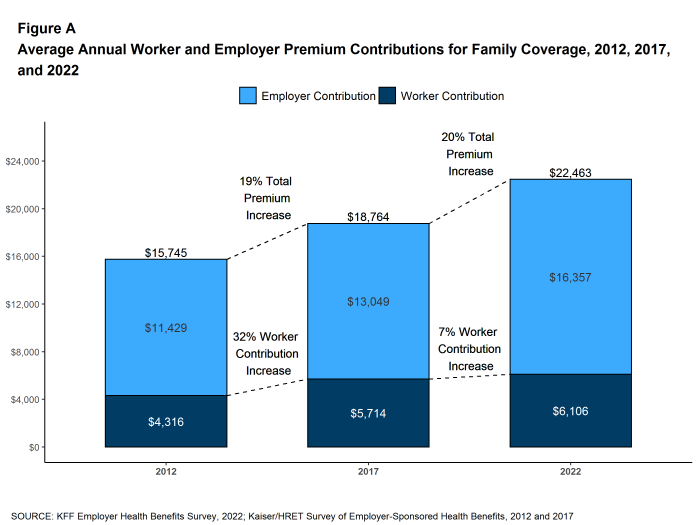

Within my annual cadence of Q4 activities has been a personal review of the KFF Employer Health Benefit Survey results; These (24th anniversary) were just posted on October 27, 2022. Click here to review the results in full. I always look forward to these survey results because they offer a unique and independent analysis of the world of employer provided employee benefits.

At our new advisory firm, we have noticed a trend towards increasing interest in leveraging the stability and cost structure of the individual market through use of ICHRA and QSEHRA plans. The objective of this blogpost is to share some information about ICHRA and QSEHRA strategies. Note that KFF also monitors the adoption rate of these strategies, though the actual adoption rate appears relatively flat over recent years.

What is an ICHRA and how does it compare to a QSEHRA?

In 2016, Congress passed enabling legislation which created Qualified Small Employer Health Reimbursement Arrangements (i.e. QSEHRA) which enabled small employers to provide reimbursement to employees for items including insurance premiums, as well as out-of-pocket healthcare costs. These plans have some limits, as described here by Healthcare.Gov.

In 2019, the Departments of Treasury, Labor, and HHS jointly published a final rule to expand use of health reimbursement arrangements (i.e. HRAs) in cases of offering reimbursement of premiums and cost sharing of certain individual health insurance policies and Medicare.

This is a general comparison of these two types of plans:

| Attribute | ICHRA | QSEHRA |

| What business can offer this HRA? | Any size | <50 w no group plan |

| Is there a cap on contributions? | No | Yes |

| Can employees have this type of HRA and premium tax credits? | No | Yes |

| Can I offer this by class (e.g. FT vs PT vs by location?) | Yes | No |

| Can the account reimburse costs related to a spouse’s plan? | No | Yes |

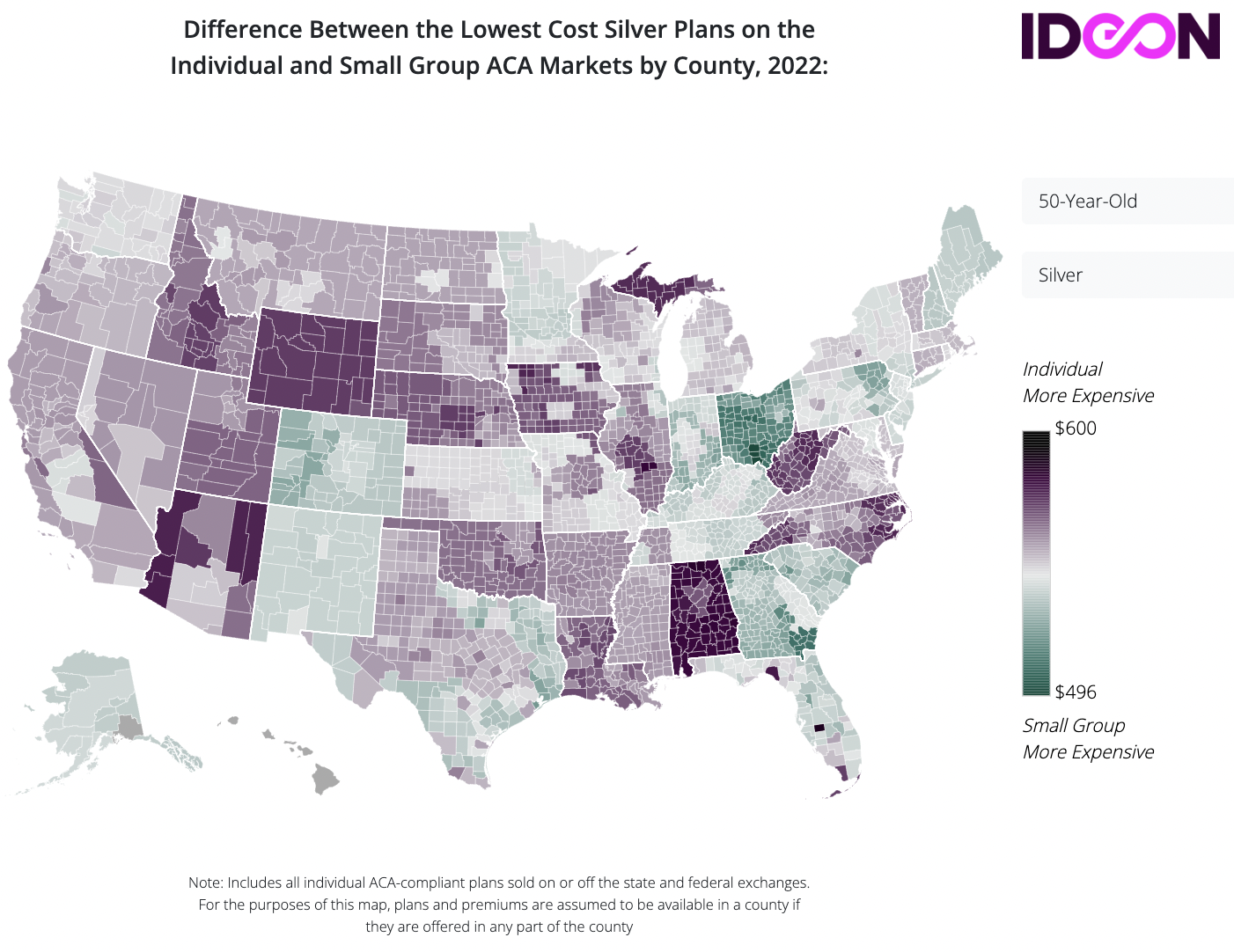

We have seen an increasing adoption of the ICHRA strategy in Pennsylvania. In reviewing strategies across multiple states, including Pennsylvania, New York, Florida, Indiana, West Virginia, Maryland, Massachusetts, and New Jersey, the (anecdotal) variation in adoption seems to track what you would expect from the following analysis of “Group vs Individual Health Insurance Costs” analysis:

Use Cases of ICHRA and QSEHRA

There are a number of ways various stakeholders may think about these strategies:

- Plan-sponsors

- Small employers

- In markets where small employee group health insurance is unattractive relative to the plans and rates available in the individual health insurance marketplace, there may be improved value to all parties made available from ICHRA and QSEHRA strategies.

- Also, in cases where small employers may operate in geographies where spousal coverage is available due to a dominant local employer (i.e. a “company town”) offering a subsidy to enable enrollment on the spouse’s plan (via a QSEHRA) may be sensible.

- Growing employers: Moving from small group to large group market

- There is risk of substantial change in premiums when moving from small group (i.e. no claims experience considered in rating) to large group (i.e. claims experience is an input to rating models); An adverse move in such a transition may be mitigated by implementing an ICHRA (noting that ACA and other compliance matters must be managed.)

- Growing employers: Focusing on geography and corporate development

- ICHRA plan designs permit for class structures based upon geography. Consequently, it may make sense to consider opportunities to leverage such a strategy in certain geographies while focusing on available group coverage in others where the fact-pattern of product and rate dynamics are supportive of purchasing those products.

- Large employers: Catastrophic levels of claims

- We are aware of larger groups that have adopted ICHRA strategies based upon persistent catastrophic claims that have limited pragmatic solutions for insurance and medical stop-loss placements. Truly, the ICHRA strategy is not limited to groups with fewer than 100 employees!

- Small employers

- Professional investors and investment bankers

- Benchmarking / diligence of EB expenditure

- When considering the relative cost and plan benefits of possible acquisitions, professional investors and investment bankers should be adding a consideration of whether an existing ICHRA/QSEHRA strategy (or lack thereof) “fits” the target fact-pattern.

- Seeking improved EV resulting from multiples on incremental EBITDA

- Given that (it is verified that) many PE professionals and investment bankers do not evaluate the possibility of incremental savings, the analysis of such strategies may present scenarios where incremental value can be revealed. Consider an example: A group of 135 employees was able to create improved employee costs and outcomes through an ICHRA and improve corporate costs by $650k; At an 8x EBITDA multiple, this group created substantial incremental value by transitioning to an ICHRA.

- Benchmarking / diligence of EB expenditure

Much of recent discussion with employers is focused on innovative solutions to create cost savings coupled with employee engagement strategies; I believe the increased emphasis on employee engagement arises from our present historically tight labor market conditions. While these strategies will inevitably not “fit” every employer, we believe they should at least be a topic of informed conversation during the time when renewal strategy specifications are being established. To discuss further, please reach out! (In addition to discussing these strategies with employers, we are also having interesting discussions with professional investors and bankers.) Thank you for reading my post!

P.S. Photo below from our trip to Colyer Lake this afternoon. It was a lovely autumn day in Central Pennsylvania!!